Covid-19 resulted in overall demand decline which has led to financial challenges for the power value chain. This in conjunction with certain announcements made by the governing bodies and the Government has aggravated the situation of these companies.

Shrinking Demand: It was expected that electricity demand and generation would be affected by the lockdown due to the restrictions on commercial, industrial and transport (railways account for approximately 500 million units demand per day) activity in the country. Further, the demand profile itself naturally shifted towards domestic usage (24.8 per cent in 2018–19) from commercial (8.2 per cent in 2018–19) and industrial (41.2 per cent in 2018–19) consumption due to people being confined in their homes. An unnatural spell of cool weather till the end of April, also kept the power demand below usual level for the period.

Shrinking Cross Subsidy: In most states, the per unit electricity rates are subsidised for domestic and agriculture consumers, to the extent that the tariff per unit is lower than the actual cost of supply. This difference in revenue generated from the industrial and commercial consumers vis-à-vis domestic and agriculture consumers coupled with shrinking demand has led to widening of losses incurred by the sector.

Shrinking Collections: The overall collections of the power distribution companies dropped on account non-payment of bills by the consumers due to cash flow challenges. To counter the difficulties faced by the consumers, State Governments have announced different schemes that further impacted the cashflow of the company.

Additionally, due to lack of manpower and logistical challenges, the Metering, Billing and Collections (MBC) Operations have been hampered and power companies have not been able to gather data from the meters installed at consumer premises. In absence of such data, consumer bills are being processed on pro-rata basis as per past consumption.

Shrinking contribution of Coal: With renewable energy projects called out as ‘must-run’, the contribution of coal to energy mix reduced from 72.5% in March 2020 to 65.6% in April 2020. Renewable energy projects run on relatively lower costs as compared to other sources. Thus, while this announcement may have attempted to cut operating costs for non-renewable projects, it resulted in piling of input material for generation of energy thus leading to blockage of working capital. As on 19th April 2020, total coal-stock with the power plants in the country has risen to 29 days as compared to 24 days on 24th March 2020.

Measures by GOI to ease the effect:

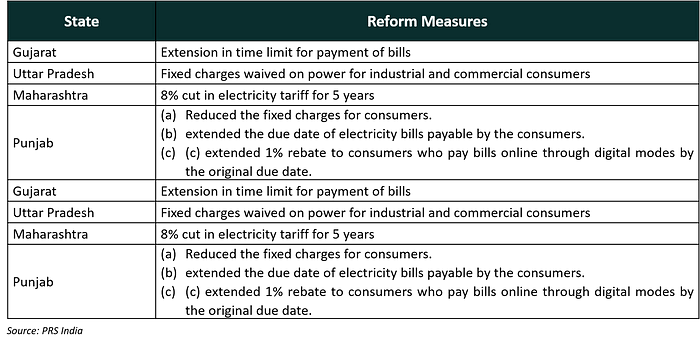

Central Government, State Governments and regulatory bodies have attempted to address the issues faced by the consumers as well as the companies through reforms such moratorium in bill payment, reduction in PSM, reduction in LPSC, cut in tariffs, priority to renewable energy and others. Key reforms included infusion of INR 90,000 crores in the electricity distribution companies. An aggregated list of announcements made can be accessed here.